How to File GST Returns The Right Way

Want to know the right method to file your GST returns. Follow along to learn more.

All business entities that are registered under GST are expected to file GST returns. The returns are filed on a monthly, quarterly, or annual basis. The filing schedule is determined by the category your business belongs to.

What is GST Return

All returns are filed through The Government of India’s GST portal. It is mandatory to add details of sales and purchases of goods and services. The taxes collected and paid for all transactions should be reported.

Enforcing A tax system like GST in India is comprehensive. This will make the tax regime more transparent and legitimate. The system comprises all taxpayer services like registration, returns and compliance. GST was enforced to get rid of numerous indirect taxes that consumers paid.

A merchant who pays taxes utilizes four forms for filing their returns. These forms include a return to suppliers, returns for the purchases done, month-end returns, as well as annual returns. Individuals are expected to update these four forms.

Small scale merchants opt for a scheme where the returns are filed quarterly. This scheme is called a composition scheme. All GST returns are filed online through the GST portal

Importance of GST Return

The GST return is a document that lists the purchases, sales, tax paid for the purchase and tax collection and other details regarding the sail. It is a document that is officially needed to be filed by all business entities and merchants as proof and ensure they don’t have any outstanding taxes.

Who is Responsible for Filing Returns?

Business entities registered under the GST council are expected to file these returns. The method and process for filing the returns vary based on the type of business you own. A list of the activities registered business entities are mandated to follow in order to file their GST returns are mentioned below

- Logs of purchases done during the taxable period

- The sales done

- List of goods and service taxes

- Input Tax Credit with GST paid on purchase.

What is the Method of Filing a GST Return Online

All business entities are manufacturers, suppliers or dealers, or customers. Anyone who runs a venture that involves active cash flow is mandated to file the GST returns every year through the portal.

All returns are filed online by utilizing the software-developed Goods and service network. With the new system, the filing of tax returns is automated. The GST portal auto-populates the details on the GSTR form

How to File your Return Online??

Step A- Log on to the GST portal. You can navigate by using the link (www.gst.gov.in)

Step B – After successful login enter the 15 digit GST identification number issue on the basis of state code and your PAN card number

Step C – Each transaction of your business will involve an invoice. These invoices should be updated with the portal. Each uploaded invoice will have a reference number issued.

Step D – After complete uploading of invoices, outward return, inward return, and cumulative monthly return must be filed online. In case of any errors that occur, one is given the option to correct it or can refile the returns. After completing the uploading of all invoices. Details of outward return, inward return, monthly return should be added

Step E – The outward supply returns should be filed in the GSTR1 form available in the information section of the GST portal. The task should be completed before the 10th of the following month

Step F – The data of the outward supplies handed over by the supplier will update in GSTR-2a and made available for the receiver

Step G – After the above-mentioned steps are completed. The receiver is supposed to check and validate the details of the outward supplies handed over by the supplier. Adding to that the details of credit and debit notes should also be validated. In case of any discrepancy, the recipient can modify the details

Step H – The recipient is expected to deliver the whereabouts of the inward supplies of taxable goods and services in the GSTR-2 form

Step I – Next, it is up to the supplier whether he wants to go ahead or hold the modifications of the details of the inward supplies made available by the recipient in GSTR-1A.In the next step, it is up to the supplier to validate the data or reject the modifications to the details of the inward supplies provided by the recipient in GSTR 1 A

Types of GST Returns about the new GST Law

1. GSTR-1

This form contains the details of the outward supplies of goods and services. The form is filled by the taxable supplier who is registered under the GST council. The buyer is expected to validate the auto-populated data and make changes if any mistakes are found

The form shall contain the following details-

- The name of the enterprise and the period for which returns are filed. It should contain the identification number of the taxpayer GSTIN.

- The invoices issued during the previous filing and the tax collected

- Advances are received because of the supply order that needs to be delivered in the future. Advanced payment received for supplies that need to dispatch in future

- Revised outward sales invoice from the previous tax periods.

GSTR-1 is required to be filed on the 10th of every month

2. GSTR-2

This form contains the details of the inward supplies of goods and services. The form is filled out by the recipient who is registered under the GST council. The supplier is expected to validate the auto-populated data and make changes if any mistakes are found.

The form shall contain the following details-

- The name of the enterprise and the period for which returns are filed. It should contain the identification number of the taxpayer GSTIN.

- The invoices issued during the previous filing and the tax collected

- Advances are received because of the supply order that needs to be delivered in the future. Advanced payment received for supplies that need to dispatch in future

- Revised outward sales invoice from the previous tax periods.

GSTR-2 needs to be filed by the 15th of the following month.

3. GSTR-3

This is a form that is filed by a taxpayer under the GST council alongside details that are auto-generated from GSTR! And GSTR2. The taxpayer can verify the auto-filled form and make changes if necessary.

- Details consisting of Input Tax Credit, liability

- Data of tax filed under CGST,SGST, and IGST schemes

- Refund claim for excess payment or authorize to carry credit forward for next filing

GSTR-3 needs to be filed by the 20th of the following month.

4. GSTR-4

GSTR 4 forms are filed by those taxpayers who have opted for the Composition Scheme which is usually opted by those with small business or a turnover of Rs. 75 lakhs. He or she must pay taxes at a fixed rate based upon the type of business.

This form contains the following details-

- The total amount for the supply during the period of return

- Log of taxes paid

- Purchase info validated by invoices

GSTR-4 needs to be filed by the 18th of the following month.

5. GSTR-5

This form is filed by taxpayers who reside out of the country. The details included in the form are

- The complete info of the taxpayer,GSTIN and period for which return is filed

- The log of outward and inward supplies

- Data of imported items during the period

- Details of import services

- Credit and debit dats

GSTR-5 needs to be filed by the 20th of the following month.

6. GSTR-6

The Form is filed by taxpayers who have put on record as an Input Service Distributor. It is mandatory to contain the following details

- Complete Data of the taxpayer consisting of the taxpayer’s name,GSTIN and period of return

- Data of Input credit that is distributed

- Details of supply accepted from registered personnel

- The amount of input credit withdrawn

- The details of the recipient of input credit

- Details regarding credit and debit

- Input tax details

GSTR-6 needs to be filed by the 13th of the following month.

7. GSTR-7

This form is filed by merchants who are registered to deduct tax at the source as per the GST guidelines. The form should contain the following data

- The Details of the taxpayer Like Name and Address

- The GST Identification Number and period for which return is filed

- The details associated with TDS, any amendments in invoice amount if present, and contact information

- Log of refunds received from electronic cash ledger

GSTR-7 needs to be filed by the 10th of the following month.

8. GSTR-8

It needs to be filed by all e-Commerce operators who collect tax at source under GST rule. It mainly comprises details of the affected supply and the tax paid during the period

Other details that it contains are-

- Name and address of the taxpayers, GSTIN, and period of return.

- TDS data and updates in the invoice and details of contract

- TDS liability is auto filled by the software

- Refund accepted from Electronic Cash Ledger.

9. GSTR-9

This form is filed by regular taxpayers accounting for all income and expenditure during a year. The associated details are regrouped every month for monthly returns.

The taxpayers are given time to make changes if any to the data in the form. GSTR9 is mandated to be filed by 31st December for the respective financial year

10. GSTR-10

The form is filed by those merchants who wish to cancel the GST registration. It should contain the following details

- The reference number for the cancellation application

- The Date when GST registration was withdrawn

- The Unique Identication

This form is to be filed by any taxpayer who opts for the cancellation of GST registration. It contains details as follows-

- Application Reference Number (ARN).

- Date of cancellation of GST registration.

- Unique ID of cancellation order.

- Date of cancellation order.

- Details of stock closure and the tax to be paid

11. GSTR-11

This form is to be filed by everyone under issued Unique Identity Number (UIN) and one that claims a refund of the taxes paid on inward supplies.

Maximize Your Online Business Potential for just ₹79/month on Lio. Annual plans start at just ₹799.

How Can Lio Help?

Lio is a small and medium-sized business (SMB) all-in-one management solution. Using Lio you can simplify accounting and inventory management, as well as banking, taxation, and payroll, so you can focus on growing your business.

Here are the steps one should take while using the Small Business templates on Lio.

Step 1: In the Item column, enter the name or description of the expense.

Step 2: Enter the value of the expense in the Amount column. The total of all expenses for the period will be automatically calculated and shown at the end of this column.

Step 3: In the Notes template, enter any extra information or notes related to the expense.

The template itself can be customized to the user’s liking by adding new columns. Simply click on the + on the top right of the template.

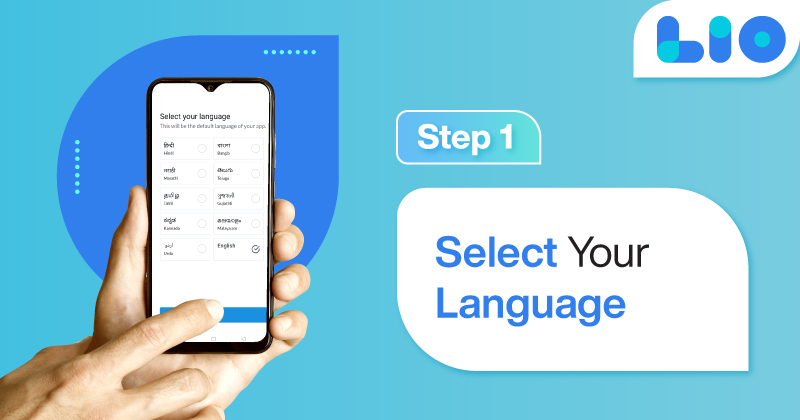

Not downloaded the Lio App yet? Here is how you can start with Lio App.

Step 1: Select the Language you want to work on. Lio on Android

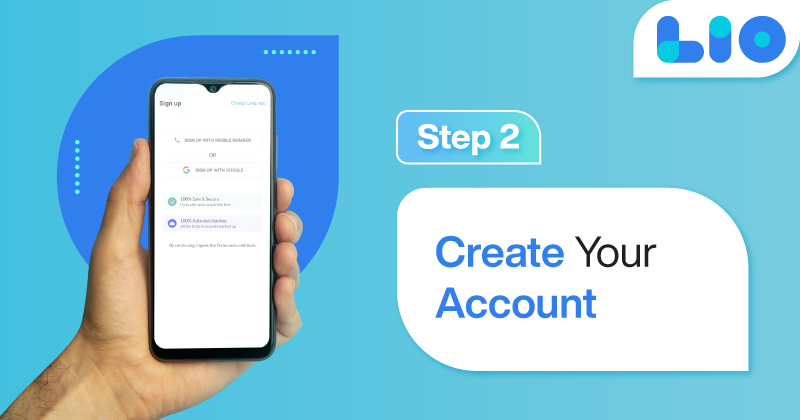

Step 2: Create your account using your Phone Number or Email Id.

Verify the OTP and you are good to go.

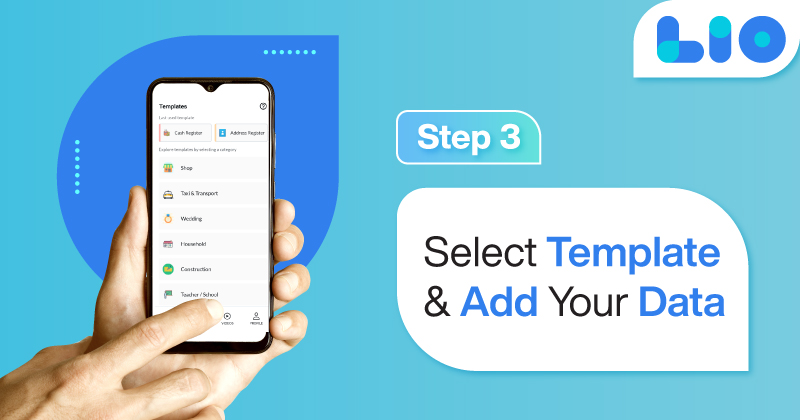

Step 3: Select a template in which you want to add your data.

Add your Data with our Free Cloud Storage.

Step 4: All Done? Share and Collaborate with your contacts.

Conclusion

Filing of GST returns is not a big deal as we have seen and come across the steps. We have even stated those steps above.

This mainly depends upon the various type of business, organization or the type taxpayers play the role.

There are different varieties to the GST files which depend on the time required, eligibility, and even certain rules and regulations. After filing the GST form the payer has to keep a check on the status of the filed GST.

If the filed GST returns is approved, you can download iy from the GST portal. A penalty will be imposed on those who fail to file their returns within a stipulated time

This penalty is also known as the late fee. As per the GST law , The fine imposed is Rs 100 for Central GST and State GST. Adding the total fine amount will be Rs 200 per day

According to the GST law, the penalty is Rs. 100 for each day for every Central Goods and Service Taxes (CGST) and State Goods and Service Tax (SGST). Coming up to a total penalty fee of RS. 200 per day.

Though this rate is subject to changes which shall be further announced via notifications. So one must be updated with the changes announced regularly.

Frequently Asked Questions(FAQS)

For what reasons can RET-1 be filed through the SMS Mode?

RET-1 form can be filed through SMS in case of NIL returns, where there is no receive or making of supplies.

In case documents are left pending, can amendments be made by the supplier to the documents?

Supplier may make changes to the data when it is rejected by the receiver and no modification is done if left pending

Can the period of filing returns be altered?

The taxpayer has a provision to change the period of tax filing once. This is possible when the first return of the fiscal year is filed

Suppose the data in the ANX1 form are updated in the wrong table can it be changed to the correct one.

The Option to change the documents into the right table is available only when they have been rejected by the receiver

What is the penalty for CGST and SGST according to the GST Law?

According to the GST law, the penalty is Rs. 100 for each day for every Central Goods and Service Taxes (CGST) and State Goods and Service Tax (SGST).

As per GST law, Rs 100 is levied as a fine for late payment for both state and central GST.

Is it possible for the taxpayers to change the period of filing of returns?

It is possible that the period of filing can be changed by the taxpayer but only once. This can only be done at the time when the first return of the financial year is filed.

6 Comments

Got to learn about the types of GST returns about the new GST law. Thank you for sharing this.

Hello Malini,

thankyou for the kind words. Glad you found the article informative.

Such an informative article! Please do write more on similar interesting topics.

Hello Nadiya,

I appreciate your warm words muchly.

I’ll certainly write more on related, fascinating subjects.

The structure of the SAP tax procedure is very confusing to me. Please advise me, if you can.

Hello Rahat,

SAP could assist you in running your company more effectively and adjusting to life after GST.

There are numerous steps in the tax configuration method, including designing an access sequence, generating a condition type, and more.

Having a thorough understanding of the configuration procedures will help you fully comprehend the process and clear up any confusions you may have.