Credit Management Guide for SMBs – Things You Must Know

Let’s face it – not all customers will be able to pay upfront for every purchase. In the interest of customer satisfaction and maintaining a good CLV (Customer Lifetime Value), businesses will have to provide flexible payment options. This mainly entails allowing customers to purchase on EMI, which is the core of Credit Management as a discipline.

Credit Management is the process of offering credit to customers, setting payment terms & conditions to enable them to pay bills on time, recover payments and ensure they comply with the company’s credit policy.

This is very important to deal with late payments and also to keep track of the business’s creditworthiness. As a small business, if customers owe more money than what the business has at its disposal, growth will become extremely difficult.

Credit Management Guide for SMBs

This article details all the best practices for credit management for small businesses to manage credit and operate the business successfully.

Check the Customer’s Credit Worthiness

Nobody wants to end up with a customer who takes too long to pay back credit or, worse, does not pay back at all. Before providing credit to a customer, their ability to pay the money back must be evaluated. Here are questions that can help ascertain a customer’s creditworthiness.

- Can the customer afford to pay the entire money owed by them within the stipulated time?

- Is the customer likely to face a financial crunch in the future?

- Are there any current indicators that point to potential problems that a customer may face in making payments?

- Does the customer have a track record of defaulting or late payments they owe to other businesses?

The answers to these questions lie in effective credit checking. These will help control the risk that comes with providing credit. The following are the most popular ways of checking the creditworthiness of a customer (this is specific to B2B customers)

- Run a Credit Report which will indicate the business’s ability to pay accounts based on its payment history and public records.

- Ask for trade references like bank statements and contacts of businesses and suppliers they had previously engaged with.

- Check the customer’s financial standing by reviewing its certified financial statements.

- Calculate their debt-to-income ratio

Decide the Terms of Credit

Once a customer’s creditworthiness is evaluated, the next step is to decide the amount of credit that will be provided to the customer and what the terms will be. Some businesses only offer credit to customers with a minimum order value. This is something that has to be considered before providing credit.

Setting a cap on the amount of credit regardless of the customer’s creditworthiness is also a safe practice. Some customers may demand a higher credit limit than what’s offered to others simply because they think they’re less risky than other customers.

It is always wise to offer smaller credit amounts to customers with low creditworthiness. SMB owners should know the profit and loss statement and ask the following questions to decide how much credit they should offer.

- What’s the credit the customer is demanding?

- What is the customer’s credit score?

- What does the customer’s payment history look like?

- What is the maximum amount the business can afford to lose if the customer becomes a bad debt?

Make sure both parties in writing formally agree upon the credit terms. . The terms should include the maximum credit period within which the customer should pay back the credit amount plus interest (if applicable).

Ease Potential Risks

Businesses, especially small and mid-size businesses, should not put themselves at financial risk by offering credit to customers for the sake of customer satisfaction. Here are some ways to limit the apparent risk associated with extending credit to customers.

For new customers, start with a reasonable credit limit. Test the waters before jumping in. See how well the business relationship grows with them and if they are making payments on time. If it is all good with them, they can be rewarded with higher credit limits.

Nobody wants a nasty surprise- especially ones that involve money. Look for patterns in the business’s financial statements (especially the sales ledger) for anything suspicious. Are there any customers who have suddenly stopped purchasing or have missed making payments?

These are tell-tale signs that they are not doing well financially at the moment. Try to get back as much money as possible from these customers before it becomes impossible to do so.

Getting insurance against bad credit is advised. This ensures that invoices will be paid for even if a customer cannot honor the credit agreement. Before taking out a trade credit insurance, research all the policies and providers available and choose the one that is best suited for the business.

If a customer asks for more credit, make sure they have paid off what they already owe before issuing more. Also, make sure to ask them to pay for the extra credit they require.

Businesses should make no clerical mistakes, such as entering the wrong name of the product or service, wrong bill amount, or even the wrong invoice number. These seemingly simple mistakes can give customers a reason not to pay back the credit they owe.

Get Invoicing Right

Invoicing should not be taken lightly. It is entirely in the business’s control, and the absence of an effective process can result in late payments. Below are the items that should be part of every invoice:

- A list with a description of goods/services with the cost of each product

- Total price (including discounts)

- The payment date as per the agreement

- Order number

- Details and instructions for payment

- Important business details like address and VAT number

Here is a sample invoice –

Customers who are large organizations usually require invoices to be sent to a specific person or a specific team within a specific date to be processed. Create and maintain a list of such people from large corporate clients.

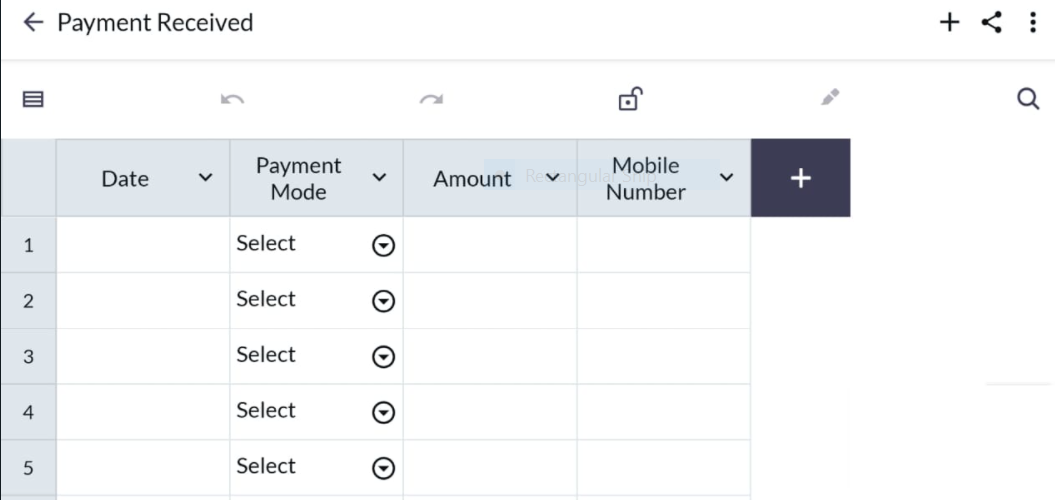

Keeping track of new and old invoices and payments is an arduous task. There are a lot of expensive cloud-based solutions in the market that can take care of this. But in all fairness, SMBs don’t need them as their money is better invested towards growing the business. All they need are the spreadsheet templates from Lio to get the job done.

For example, the Payment Received template can help keep all received payments in one place. Another template called the Order Book Register helps manage all order lists and customer records. Given below are screenshots of both.

Payments Received

Order Book Register

Also Read: Top Free Inventory Management Software You Can Use

Conclusion

It should worry all businesses if they notice that they are owed more money than what they have as liquid cash. It’s like having something you don’t have. The points discussed above can, to a large extent, help businesses get a better grip on credit management.

I hope you have enjoyed reading this article on credit management and have learnt all about it.

6 Comments

Top-notch work! Leaned so much about credit management for SMBS.

Hi Yask,

I am glad that you liked the article. Stay tuned for more such articles. Happy reading.

Would you kindly provide me with a brief list of the different credit management techniques?

Hello Meghana,

There are essentially seven credit management strategies to take into account. These are some practices that can help you perform better while saving time.

1. Conduct routine credit checks

2. Tighten credit conditions for picky clients

3. Transmit invoices online

4. Schedule polite calls

5. Invest in training

6. Give bills top priority

7. Work with a debt collecting company

I enjoyed this article so much. Could you help explain what O2C is to me?

Hello Vysakh,

A collection of business procedures known as order to cash (OTC or O2C) involve receiving and completing consumer requests for products or services. Management uses this top-level, context-level term to refer to the financial aspect of customer sales. The order-to-cash (O2C) process is crucial to a business’s performance and is a major factor in how well an organization treats its customers.

I hope I was clear.