All about Debit Notes and Credit Notes you should know about

Are you searching for an answer about the debit notes and credit notes? Well, you have landed on the right article because it is full of some important pieces of information about the same.

Debit and credit notes are both official documents of accounting that are used by businesses but for different purposes. They are similar to invoices but are not invoices as it lets the buyer know about the existing business credit they have or they still owe.

All businesses use debit notes and credit notes for accounting sales and purchase returns as official documents. These notes actually help the buyer to know how much they owe and how much credit they have.

For businesses that deal with both debit notes and credit notes, it becomes important for them to understand it but the understanding also varies from buyer to seller.

Basically in the invoices or bills in a business that are used to maintain a record, when the values change after a proper bill is made, you do not edit that.

The generated transactions and records cannot be changed hence one makes additional entries that show these changes in the original document and are further proof of the actual value. These new records are called debit and credit notes.

What Is A Debit Note?

A debit note is issued as a request by a buyer on receiving damaged services or goods from a seller. This is considered a formal request to the seller from the buyer to issue a credit note.

It is also known as a debit memo and can be issued to the seller by the buyer requesting the return of the whole or partial amount of payment already made. This could be due to damaged or incorrect goods received or even the cancellation of the order or any other circumstances.

This is basically the evidence of purchase return that is maintained in the buyer’s account. Whereas a credit note acts as proof of a sales return and is issued when as a customer you receive services and goods that might not match the expected standard while you are in receipt of the final invoice from the seller.

When Can A Debit Note Be Issued?

A buyer can issue a debit note under the following circumstances:

- Wrong tax rates have been declared in the context of the goods in the tax invoice

- A supplier/seller has valued the goods at the wrong value which is less than the actual value in the tax invoice

Definition Of Debit Note As Per GST

As per Section 34(3) of the GST Act, “Whenever any tax invoice has been issued for the supply of any goods or services or both of them and the taxable value or charged tax in that invoice is found to be less than the taxable value or payable tax in respect of such supply, the registered person, who has supplied such goods or services or both, is bound to issue to the recipient a debit note containing such particulars as may be prescribed”.

Common Reason For Issuing Debit Note

- The purchaser was over-billed

- A damaged or defective product received

- Incorrect amount in the invoice

What Is A Credit Note?

Also known as a credit memo, a credit note is a document that is issued by the seller. A credit note is issued because of the supply of damaged goods or when they are returned or due to an error that occurred in the bill.

It shows the partial or full return of money or funds that are raised in response to the buyer’s debit note. There are two types of credit notes issued; incoming payments and outgoing payments.

When Can A Credit Note Be Issued?

A credit note can be issued when:

- There is an error in the invoice.

- The quality of the product is not up to the expectation of what a buyer wanted.

- The quantity received by the buyer is not the same as written in the invoice

Definition Of A Credit Note As Per GST

According to the Section 34 of the Goods and Service Tax, “Whenever a tax invoice has been issued for the supply of any goods or services or both of them and the taxable value or charged tax in that tax invoice is found to exceed the taxable value or payable tax in respect of such supply, or when the goods supplied are returned by the recipient, or when goods or services or both of them supplied are found to be somewhat deficient, the registered person, who has supplied the goods or services or both, must issue to the recipient what is called as a credit note mentioning the prescribed particulars”.

Common Reason For Issuing Credit Note

- Corrections in already issued invoice

- Cancelling any pending payments against the invoice

- On the return of a damaged or defective product by the consumer, you can issue a credit note for adjustments against the already raised invoice.

Debit Notes And Credit Notes As Per GST

Following are the reasons specified in GST for which both debit notes and credit notes can be issued:

- Deficiency in services

- Sales return

- Correction in invoice

- Post sale discount

- Finalization in provisional assessment

- Change in POS

Details To Be Included In A Debit Notes And Credit Notes

By now we have understood that the debit notes and credit notes are issued when a buyer returns the goods back to the seller because of the reasons mentioned above. Below mentioned are the details that are to be included in debit notes and credit notes:

- Name, address of the supplier and GSTIN of the supplier

- Name, address, GSTIN (if registered) of the recipient

- Date of issue

- An alphanumeric document serial number unique for the financial year

- The taxable value of the goods/services, the applicable rate of tax, amount of tax credited or debited to the recipient.

- The invoice number that the debit or credit note is being issued against.

- A seal/stamp and signature of the supplier.

Also Read: How to change Trade Name in GST Portal?

Debit Notes Vs Credit Notes

So what are a debit note and credit note in short? A Debit Note is a document that shows that a debit is made to the other party’s account. A credit note is an instrument that is used to inform that the customer’s account is credited in his books.

Now that we have understood both debit and credit notes individually, let us look at the difference between the two of them and how they are different from each other. It becomes important to understand the difference between these two as one would have to frequently use them in various scenarios.

Difference Between Debit Notes and Credit Notes

The table below will show you the main differences between credit and debit notes.

| Who issues it? | Issued by the buyer of goods. | Issued by the seller of goods. |

| What does it mean? | The debit note is issued to the seller by the buyer to return the goods received because of quality issues or any other reason. | The credit note is issued by the seller of goods to confirm that the purchased return is accepted. |

| Can be issued | Only in the event of credit purchases from the buyer's perspective. | Only in the event of credit sales. |

| What is the impact? | It reduces account receivables in the books of sellers. | It reduces account payables in the books of the buyer. |

| Reflects | A debit note reflects a positive amount. | A credit note reflects a negative amount. |

| Form | It is another form of purchase return. | It is another form of sales return. |

| Accounting | It leads to updating purchase return books. | It leads to updating of sales return books. |

| Entry | Supplier Account Dr. Purchase return Cr. | Sales return account Dr. Customer Account Cr. |

| Issued in exchange of | Issued in exchange for a credit note. | Issued in exchange for a debit note. |

| Issued by a seller to the buyer | The seller issues debit notes to the buyer if the buyer is undercharged or the seller has sent additional goods. | The buyer issues a credit note as an acknowledgement of a debit note received. |

| Ink | It is issued in blue ink. | It is issued in red ink. |

Purchase Return Is Debit Or Credit?

A purchase return is something that occurs when a buyer sends the goods back to the seller because of something problem or the other. Excessive purchase returns can affect the profitability of the business hence purchase returns must be very closely monitored. There are a number of reasons why purchase returns can happen and they are as follows:

- Buyer got wrong goods

- Goods are inadequate in some way or the other

- The seller sent the wrong goods

- The buyer initially bought an excessive quantity and now wants to return the remaining products.

A purchase return is basically an account that is maintained when a buyer returns a product back to the seller. Since the return of the purchased goods can be time-consuming hence an account purchase return would be maintained under the periodic inventory system.

The credit balance in this general ledger account is used to offset the debit balance of the account.

This means that purchase return is credited in the book of accounts. Let us now look at the advantages of purchase return journal entry:

- It helps in keeping track of return transactions.

- It helps reduce the balance of return transactions from the total inventory.

Sales Return Is Debit Or Credit?

Sales return is debited in the account books and is taken as a contra revenue account. So let us understand what is a sales return. Sales return is the product sent back by the consumer to the seller.

The return usually happens when the buyer gets a defective product or it is bought in abundance and now he wants to return the remaining. The other reasons can be that the product was delayed, was incorrect or either the product specifications were not right.

And when the buyer finds these problems, he would want to send the product back to the seller and would ask for reducing the credit balance or returning cash or reducing the credit balance.

This return is recorded as a debit by the seller to a Sales return account and as a credit to the accounts receivable account.

The fundamental goal of sales return accounting is to revise previously recorded revenue and the price of products sold. Accounts receivable, as well as cash equivalents and cash, must influence whether a sale is made in cash or on credit.

Maximize Your Online Business Potential for just ₹79/month on Lio. Annual plans start at just ₹799.

How Lio Can Help With Debit And Credit Notes?

For the apt organization of your business data, Lio provides tools for easy tabulation and calculation of your debit and credit notes. It is a very simple yet very powerful app to use especially by business owners so that all their data is in one place.

You can analyze your transactions, keep track of the day-to-day activities of the business and get information about what goods are to be returned and sold according to the tabular datasheet so that it is easy for you to issue debit and credit notes.

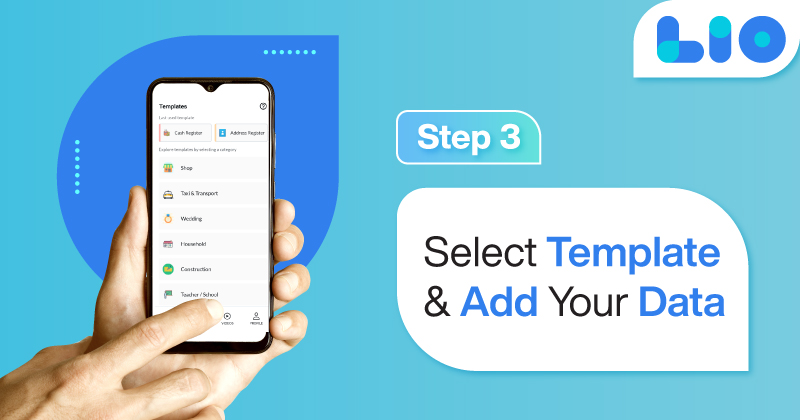

Not downloaded the Lio App yet? Here is how you can start with Lio App.

Step 1: Select the Language you want to work on. Lio for Android

Step 2: Create your account using your Phone Number or Email Id.

Verify the OTP and you are good to go.

Step 3: Select a template in which you want to add your data.

Add your Data with our Free Cloud Storage.

Step 4: All Done? Share and Collaborate with your contacts.

With these simple steps, one can easily make use of the Lio application for the Debit and credit notes in their business and have a smooth running of the work related to it.

Conclusion

Hope by now you have understood that the debit note is a method by which the value of the goods or services in the original tax invoice is improved due to some errors. On the other hand, by issuing credit notes the value of goods and services is revised.

Under the issuance of the debit note, the seller pays the tax liabilities and in the credit note, the tax liability decreases. The above article provides information about these legal methods and some details about by whom and for what they are issued. Some frequently asked questions are also mentioned for a better understanding of the debit and credit notes.

Frequently Asked Questions (FAQs)

What is the main difference between a Debit and a Credit Note?

A debit note is issued by a buyer when returning purchased goods while a credit note is issued by a seller during sales returns.

In how many days of Purchase can a Debit Note be issued?

The buyer can issue a debit note within 30 days of the purchase date mentioned in the invoice.

What are some details that need to be mentioned in these Notes?

Issuer’s details and GSTIN, recipient’s details and GSTIN, date of issue of the note, date of the original invoice and unique number given to the note.

Can a single Credit Note be issued for Multiple Invoices?

Yes, an individual can create a consolidated credit note that can be issued for multiple invoices.

Are Debit Notes and Revised Invoices the same?

No, the former is issued while returning goods whereas the latter is made when there is an issue in the invoice.

Is Debit Note Debited or Credited?

A debit note is debited.

Give an example of a Credit Note?

In the credit note, the negative balance of an invoice is shown. For example, if the seller has invoiced a customer for a sum of INR100 and the customer now wishes to cancel the whole invoice, the seller would have to issue a corresponding credit note for the negative value of -INR100.

6 Comments

This article has really opened my eyes. got to gain knowledge of the definitions of debit and credit notes, as well as their differences. I’m definitely going to tell my friends about this.

Hello Adnan,

I really appreciate your warm words.

I’m happy you found this article informative and helpful.

Absolutely, spread the word to your friends.

Have fun reading!

Could you help explain why credit notes are referred to as credit memos?

Hello Rahul,

A credit memo is an abbreviation for “credit memorandum,” which is a document issued by the seller of goods or services to the buyer that reduces the amount owed to the seller under the terms of an earlier invoice. A credit note, also known as a credit memo, is a business document issued by a seller to a buyer.

This app is awesome! It is really versatile. Numerous languages, a lock option, options for color coding, and more.

Hello Goury,

I really appreciate your warm words.

I’m delighted the Lio App captured your attention.

Feel free to explore the app and let us know what you think.