Advantages and Disadvantages of GST: A Detailed Study

By now, all of us are familiar with the Goods and Services Tax (GST). But what are the advantages and disadvantages of GST? That is a question that not many still have answers to. This article aims to address that along with many other questions you have in mind related to GST. But first-

What is GST?

GST is a single form of tax that is applicable all over the country. Under this regime, a tax is charged at each point of sale.

The Goods and Services Tax Network (GSTN) has jointly been set up by the central and state governments to help implement GST by providing three front end services:

- Registration

- Payment

- Returns to taxpayers

What’s the objective of GST?

The following are the primary objectives of GST:

- Eliminating cascading taxes: Under GST, taxes are levied only on the net value-added. This lowers the cost of goods by eliminating the tax-on-tax regime.

- Clubbing of indirect taxes: Almost all the indirect taxes under the state and central government are now clubbed under GST

- Increase revenue surplus and tax to GDP ratio: A high tax to GDP ratio means higher tax collections. This is an indication of a strong economic system. The government can improve the income from taxes through a wider tax base and increased tax compliance.

- Decreased corruption and tax evasion: Since there is only a single tax, the chances of people evading taxes or providing wrong information are considerably reduced.

- Better tax compliance: Due to its simple nature, GST ensures that a large number of businesses, especially the small and unorganized ones, comply with the tax regime.

- Better efficiency and productivity: The GST is also instrumental in removing all constraints tied to logistics and the unusually lengthy process of the input tax credit. Organizations benefit from improved overall productivity because GST takes over entry tax.

Let us now look into the advantages and disadvantages of GST.

What are the advantages of GST?

The following are the advantages of GST over the complicated tax regime that preceded it. Some of these were briefly mentioned in the sections above. Let us probe a little further.

Eliminating the tax on tax

One of the most obvious and important benefits of GST is the unification of multiple taxes (both state and central) under the same roof. It removes multiple taxes on the same product and improves the flexibility of tax processing. Let’s understand this better with an example:

Pre GST: Suppose Govind, a hotel owner charges ₹ 10,000 for a 5-day stay at his hotel. The service tax he has to pay will amount to ₹ 1500, i.e., 15%. They also sold some toiletries worth ₹ 5000, for which he had to pay a VAT of ₹ 250. That is, the total tax paid by him would amount to ₹ 1750.

Post GST: The new service tax amount for Govind under the GST regime will be ₹ 1800 (18%). The tax deducted on toiletries will be credited back to Govind. So, the net tax amount will be ₹ 1550 (1800-250).

Better threshold limit

Before GST was implemented, businesses had to pay VAT (Value Added Tax) after the ₹ 5 Lakhs mark. The amount also varied from one state to another.

Now, in the GST era, the threshold has been increased to ₹ 20 Lakhs. This came as a massive relief for up-and-coming small and medium-sized businesses.

Minimized compliances

Earlier, there were separate compliance rules for each tax. For example, excise tax returns were filed each month. Companies and Limited Liability Partnerships had to file taxes monthly.

It was quarterly in the case of partnerships and proprietorships. The period for filing VAT was also not fixed before GST came into the picture. Now, taxpayers should only file returns once.

Use the Composition Scheme to pay GST at fixed rates

GST has a provision to lower taxes for businesses. If a business’s annual turnover is between ₹ 25 Lakhs and ₹ 75 Lakhs it can go for the Compensation Scheme to minimize the taxable income.

This scheme enables the payment of GST at a fixed rate irrespective of the level of income as long as it is within the bracket mentioned above.

Easy online processing

Filing taxes was always a pain in the pre-GST era. Post the introduction of GST, it has become an extremely simple and straightforward process to file taxes. Even someone with very basic knowledge of computers can do it.

All that needs to be done is to create an account in the GST portal, log in and start filing returns. All necessary details and guidance for filing tax returns are available on the portal itself.

The biggest beneficiaries here are start-ups. Due to its online nature, it is easy to establish transparency among tax jurisdictions between the central and state governments.

Warehousing simplified

To waive off Central Sales Tax during the pre-GST era, companies used to set up multiple warehouses.

Most warehouses were also far below the optimum capacity because of the non-availability of many products. Now with GST in place, companies can set up warehouses at locations that are optimal for their operability.

As a result, these companies can cut a lot of unnecessary costs. It has also forced a lot of businesses in the unorganized sector to comply with tax regulations.

Takes e-commerce into consideration

E-commerce sellers were not really under any law before GST came into the picture. They were charged at variable rates under many tax schemes. Every state had separate provisions, and this made things very confusing and laborious for everyone involved.

E-commerce sellers were not required to pay any VAT in some states like Rajasthan and West Bengal because they were treated as mere mediators in those states.

While in Uttar Pradesh, they were treated as VAT compliant firms. With the implementation of GST, such complexity has been removed as e-commerce companies are treated as separate entities.

A common national market

There has been a significant and steady rise in the country’s GDP since the introduction of GST. We are looking at economic efficiency in the long run.

This tax regime is leading to uniformity among different sectors and eradicating economic distortion, forming a common national market.

What are the disadvantages of GST?

Yes, GST is a blessing in disguise for businesses across the country. But it is not without its flaws. Here are the top 10 disadvantages of GST –

The increased cost of operation

When GST was implemented, businesses could no longer rely on traditional books and accounting. They had to make an expensive switch to the latest GST compliant Enterprise Resource Planning (ERP) software to keep the business running.

This software is expensive, and, in most cases, users will require training to learn to operate them properly – an additional cost. Generally, GST has increased the total cost of operation for a lot of small and medium-sized businesses, and they usually must hire a professional to assist them with matters related to GST.

Not applicable on petroleum products

Petroleum products are exempted from GST but attract other taxes like central excise duty and VAT levied by states governments.

Increased tax liability on businesses

As per the GST regime, businesses with a minimum turnover of ₹ 40 Lakhs must pay taxes. This came as a huge blow to a lot of businesses because the minimum turnover in the pre-GST era was ₹ 1.5 Crores.

The burden of compliance

The GST scheme mandates that every business must register themselves on the GST portal in the state of their operation. The whole process can sometimes prove to be very tiresome.

This has added even more pressure and paperwork for businesses in India that are already dealing with too many bureaucratic hurdles.

On top of this, most people are not that savvy when it comes to the adoption of technology, making things even more difficult for new businesses.

Penalties for non-compliance

Non-compliance with the rules of the GST regime will attract hefty penalties for businesses. In all fairness, it will be difficult for most small and medium enterprises to understand the intricacies of GST. They will be forced to hire a professional to help them out.

It came into effect half a year in

GST came into effect on 1 July 2007. So, businesses followed the old tax structure from April to June and then switched to GST from July. This led to a lot of confusion as some companies were doing taxes parallelly.

Online tax regime

The GST Regime is a completely online tax system from registering to filing returns. While established businesses could quickly adjust to this new system, smaller businesses were not very well versed with such modern solutions.

Impact on the real estate market

Since the implementation of GST, the real estate market has witnessed an 8% increase in prices which has subsequently led to a 12% decline in demand.

Hit on the telecom industry

The Indian telecom industry faced many challenges when GST was introduced. The implementation itself was difficult because of a lack of clarity on certain issues.

To comply with GST regulations, telecom providers had to go through a complete redesign of IT infrastructure and payment systems, which led to a lot of additional costs.

Not explorer-friendly

Critics have pointed out that GST gives undue preference to the informal sector – neglecting the growth of large companies.

And that wraps up the disadvantages of GST. Now that we have seen both the advantages and disadvantages of GST, let us look at the other aspects of it.

Who is taxable and who should be registered under GST?

Under GST, a taxable person is anyone who runs a business in India and is required to register or has already registered under the GST Act. Anyone involved in economic activity is considered a taxable person.

The word ‘person’ includes individuals, HUF, company, firm, LLP, any corporation/government entity, an AOP/BOI, a corporate body incorporated under laws of a foreign country, cooperative society, local authority, trust, government, and an artificial juridical person.

The following entities are mandatorily required to register under GST:

- Any business engaged in the supply of goods whose turnover for a financial year exceeds ₹ 40,000,00 for the Normal Category States and ₹ 20 Lakhs for the Special Category States

- Any business engaged in the supply of services whose turnover for a financial year exceeds ₹ 20,000,00 for Normal Category states and ₹ 10 Lakhs for the Special Category States

- Every person registered under the previous law (Excise, VAT, Service Tax, etc

- When a registered business has been transferred to someone or demerged, the new owner shall register the business with effect from the date of transfer.

- A person making inter-state supplies

- Casual taxable person

- Non-resident taxable person

- A supplier’s agent

- People paying tax under the reverse charge mechanism

- Input service distributor

- E-commerce companies

- People who supply via an e-commerce aggregator

- Persons supplying online information and database access or retrieval services from outside India to persons in India, other than a registered taxable person

How to Register for GST?

Important points

- A person has to apply for registration in every state in which he/she is liable, within 30 days from which they become the liable person.

- Casual/non-resident taxable persons should apply at least five days before business commences.

- Having A PAN (Permanent Account Number) is a prerequisite for getting registered.

- The assessee must get separate registration for each state since registration under GST will be state-wise.

- The assessee must get separate registration for each business vertical in the same state.

This section of the blog discusses the steps one should take to register for GST, the documents required for it, etc. Let us get into it.

The procedure

Applicants can initiate the registration process on the GST portal. Once the application is submitted, applicants will instantly receive the ARN Status.

Using this ARN, applicants can check the status of their application and post queries if needed. Applicants typically need to wait no more than a week to get their GST Registration Certificate once they’ve generated their ARN.

Required Documents for GST Registration

The following are the documents needed to complete the GST registration process.

For sole proprietor or individual:

- PAN address

- Address proof

- Photographs

- Aadhar card

- Bank account

For partnerships including LLP:

- PAN

- Address proof

- Bank account details

- Copy of partnership deed

- Registration certificate on board resolution (for LLP)

- Photographs of authorized signatories and partners

- Proof of appointing authorized signatory

For HUF:

- PAN

- Address proof

- Details of bank account

- Owner’s photograph

- Aadhar card and PAN card of the Kartha

For Companies:

- PAN Card of the company

- Bank details

- Address proof of the principal place of business

- PAN and Aadhar of authorized signatories

- PAN and address proof of directors of the company

- Articles of Association or Memorandum of Association

- Proof of appointment of authorized signatory

- Certificate of incorporation issued by the Ministry of Corporate Affairs

Registration Fee

There is no fee charged if an applicant decides to register online through the GST portal. But, if they wish to get help from a GST practitioner or a Chartered Accountant, there will be a fee as laid out by the service provider.

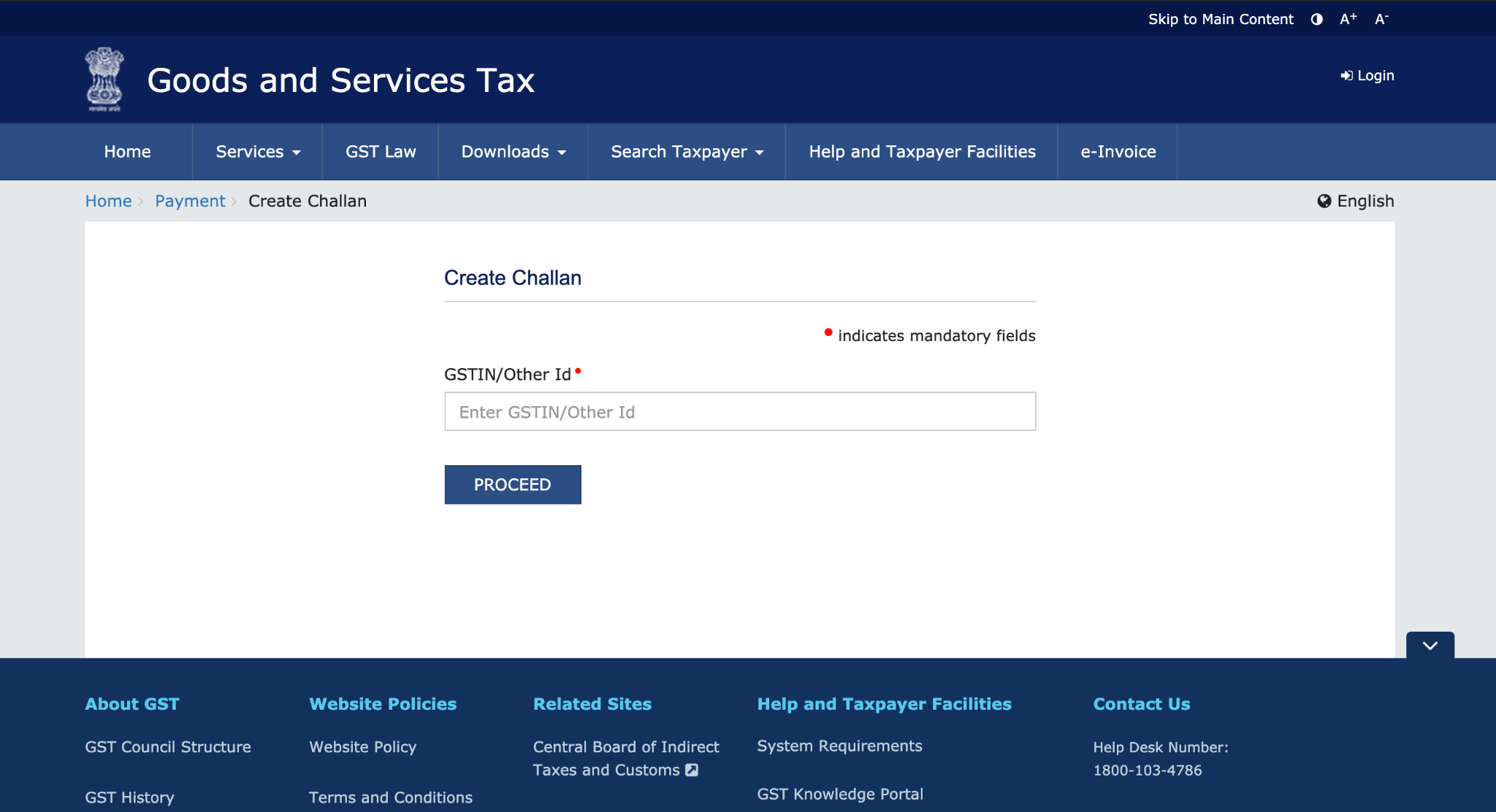

How to pay GST?

All challans have to be prepared by taxpayers on the online GST portal. This is done to ensure that bank employees don’t enter the wrong information on physical challans.

Once the challans are generated, taxes can be paid using either of the below options:

- Online using the GST portal through any bank authorized by the RBI to collect payments. This can be paid through Net Banking or using a credit/debit card. The paid challan can then be directly downloaded from the portal.

- Over the Counter by printing the challan and getting it processed at an authorized bank as cash or cheque. After the payment is approved, the bank will transfer the money to the RBI and send a confirmation of payment to the GST Portal for accounting.

GST Slabs

There are four slabs in India. It has been structured in such a way that food items and essential services are in the lower bracket while the higher bracket is composed of luxury products and services. Over 1300 goods and 500 services are spread across four slabs of 5%, 12%, 18%, and 28%.

| Under the 5% Slab | Under the 12% Slab | Under the 18% slab | Under the 28% slab |

| Goods: Apparels under ₹ 10,000 | Agarbatti | Braille items (watches, paper, typewriters) | Coir mat | Cashew nuts | Domestic LPG | Edible oils | Floor covering | Fish fillet | Fertilizers | First-day covers | Frozen vegetables | Footwear up to ₹ 500 | Hearing aids | Insulin | Milk-based food items for babies | Medicines | Matting | Packed paneer | Packaged food items | Pizza bread | Postage stamps | Roasted coffee beans | Revenue stamps | Rusk | Sugar | Stent | Skimmed milk | Tea | Stamp-post marks | Sabudana, etc. Services: Road transport by cabs and radio taxis | Supply of tour operator’s services | Restaurants with a turnover of up to ₹ 50 lakhs | Economy class air travel | Sale of advertisement space | Transport services including railways and airways, etc. | Goods: Ayurvedic medicines | Almonds | Apparel above ₹ 1000 | Animal fat sausage | Butter | Bhujia | Chutney | Chessboard | Carrom board | Cake server | Reagents and diagnostic kits | Exercise books | Fruits | Frozen meat products | Fish knives | Forks | Fruit cakes | Glasses for spectacles | Ghee | Jam | Jelly | Mobile phones | Namkeen | notebooks | Non-AC restaurants | Pickle | Packed coconut water | Sewing machine | Tongs | Toothpowder, etc. Services: Hotels | Guest houses | Inns with tariff between ₹ 1000 and ₹ 2500 per night | Business class tickets, etc. | Goods: Aluminium foil furniture | Biscuits | Bamboo | Branded clothing | CCTV | Cameras | Cakes | Corn | Curry paste | Envelopes | Footwear priced over ₹ 500 | Hair oil | Instant food mixes | Ice cream | Mineral water | Mayonnaise | Monitors | Padding pools | Pasta | Printers | Preserved vegetables | Soups | Soaps | Salad | Dressing | Steel products | Tissues | Tampons | Toothpaste | Weighing machines, etc. Services: Telecom services | AC hotels that service alcohol | IT services | Hotels that range between ₹ 2500 and ₹ 5000 per night, etc. | Goods: Aerated water | Private aircraft | After shave | Motorcycles | Ceramic tiles | Deodorants | Dye | Hair shampoos | Paan masala | Paint | Shaving cream | Shaver | Water heater | Washing machine, etc. Services: 5-star hotels | Gambling and betting in race clubs | Hotels that charge more than ₹ 5000 per night, cinema and entertainment, etc. |

Goods and Services Exempted From GST

Due to many socio-economic conditions, many goods and services were always exempted from the past taxes. For example, clinical and educational services were exempted from service tax. Like that, there are also exemptions under the GST regime. Here are they –

Exempted supplies

- Petrol

- Alcohol

- Supply of goods to Special Economic Zones (SEZ) or an SEZ developer

- Supply of goods that comes under a zero-rated list. For example, vegetables, fresh milk, etc.

Exempted goods

- Foods: Fruits, vegetables, cereals, meat, fish, potatoes and other roots, tender coconut, tea leaves, jaggery, curd, ginger, coffee beans, etc.

- Raw materials: Silk waste, raw silk, raw jute fiber, handloom fabrics, unprocessed wool, cotton for khadi yarn, khadi, firewood, charcoal, etc.

- Tools and Instruments: Shovels, spades, agricultural tools, handmade musical instruments, hearing aids, and other tools used by differently-abled individuals.

- Miscellaneous: Contraceptives, human blood, vaccines, organic manure, earthen pots, beehives, maps, books, journals, pooja props, kites, newspapers, etc.

Exempted services

- All services related to agriculture – harvesting, supply, cultivation, packaging, warehouse, renting or lease of machinery, etc. This list does not include the rearing of horses.

- Transportation of individuals via public transport, cabs, auto-rickshaws, metro trains, etc.

- Transportation of goods where the total charge is less than ₹ 1500.

- Government and foreign diplomatic services

- Services provided by RBI or any foreign diplomatic mission

- Services provided to diplomats, including those from the United Nations

- Certain healthcare and educational services like mid-day meal catering services, services provided by a Vet, clinics, paramedics, charities, and ambulances.

Some other exemptions

- Services provided by tour guides to foreign tourists

- Libraries

- Services specializing in religious ceremonies

- Distribution of electricity

- Services by authorized sports organizations

How to calculate GST ?

GST is calculated as the sum total of GST payable on reverse charge, output supplies, and inward supplies. This total is individually derived for each month and has to be paid while filing GST returns on a monthly basis.

Taxpayers have to consider all aspects and charges, including reverse charge, exempted supplies, interstate sales, etc. Getting the calculation right is essential to avoid paying the 18% interest that will be charged if the payment is below the actual amount due. To get an indicative amount of tax liability, please use the calculator available on the GST Portal.

The Calculation Formula is-

Amount of GST = (Original Price x GST Rate) / 100

Net Price = Original Price + Amount of GST

What account should be maintained for GST?

Under the GST regime, a trader has to maintain the following accounts on top of the usuals like purchase, sales, etc.

- Input CGST

- Output CGST

- Input SGST

- Output SGST

- Input IGST

- Output IGST

- Electronic cash ledger (on the GST portal)

All but the last one can either be maintained either using expensive software or building custom templates using excel. Or, the best option would be to download the free GST Register template from Lio. Just download the app and navigate to Shop on the homepage.

When should you file GST Returns?

The GST Return or GSTR as it is called should be filed by taxpayers with the concerned authorities.

The GSTR comprises details of income, sales, expenses, and purchases – proving useful in computing the tax liability of an entity. Registered dealers have to file GSTR inclusive of the following:

- Sales

- Purchase

- Output GST

- Details of Bank Account

- Input Tax credit

Regular business with a turnover of more than ₹ 5 Crores must file one annual return and two monthly returns, i.e., 25 returns in one year. However, under the Quarterly Return Filing and Monthly Payment (QRMP) scheme, the number of GST returns varies for that whole file quarterly GSTR-1.

If such is the case, taxpayers have to complete nine GST service tax returns in a year which includes the annual return and GSTR-3B. The number also varies for special cases like composite dealers – who must file for returns five times in a year.

New compliances

The following are the new systems the GST regime has introduced along with the filing of returns online:

E-way bills

This was introduced for the inter-state movement of goods on 1 April 2018 and for the intra-state movement of goods on 15 April 2018.

Through this centralized system, traders, manufacturers, and transporters can effortlessly generate e-way bills for transported goods. It has also come as a boon for tax authorities by decreasing time at check posts and has also proven to be effective in reducing tax evasion.

E-invoicing

The GST bill system is applicable for businesses with an annual turnover of over ₹ 100 crores in the previous fiscal year. Businesses of this nature should obtain a unique invoice reference number for B2B invoices.

The way to get this is by uploading the invoices on the GSTN’s online invoice registration portal, which will verify the accuracy and authenticity of the invoices before generating the reference number. Reduction of data entry errors and better inter-operability of invoices are the biggest advantages of e-invoicing.

HSN code requirements

From 1 April 2021, it is mandatory for businesses to mention their HSN/SAC code to all supplies of goods and services on tax invoices.

GST Council Meetings

Since its constitution, the GST council has met thirteen times. Some of the most important decisions take in the council meeting are:

- Rules for the conduct of business in the GST council

- Timetable for GST implementation

- The threshold limit for exemption from levy of GST would be ₹ 20 Lakhs for states (except for special category states)

- The threshold for availing of the Composition scheme would be ₹ 50 Lakhs. Service providers and some others will be kept out of the Composition Scheme.

- To compensate states for 5 years for loss of revenue due to GST implementation, the base year for the revenue of states will be 2015-16, and a fixed growth rate of 14% will be applied to it.

- Approval of the draft GST Rules on registration, payment, return, refund and invoice, credit/debit Notes with the consideration that minor changes may be permitted with the Chairperson’s approval if required based on suitable suggestions from the stakeholders for from the law department.

- All parties exempted from paying indirect taxes under any existing tax incentive scheme would pay tax in the GST regime. The decision to continue with any incentive scheme shall be with the concerned State or Central governments. In case the government decides to continue with any existing exemption or incentive scheme, it will be administered through a reimbursement mechanism.

- Adoption of four slabs tax rate structure of 5%, 12%, 18% and 28%. There will also be a category of exempt goods, and a further cess would be levied on goods like luxury cars, aerated drinks, pan masala, etc., over and above the rate of 28% for payment of compensation to the states.

- GST rates on 1211 items were approved at the 14th GST Council Meeting held on 18 and 19 May 2017.

- At the 15th GST Council meeting held on 3 June 2017, tax rates of the remaining goods were approved.

- 22 states and 2 union territories with Legislatures have already passed their respective State GST bill

- The issue of cross empowerment and administrative division of taxpayers between the Centre and State governments has been resolved.

Developments in 2021

September

The GST Council is considering taxing petrol, diesel, and other petroleum products under the GST regime. This move will require significant compromises from both the central and state governments.

This is seen as a viable solution to the almost record high petrol and diesel rates the country is seeing right now, as it will end the cascading tax effect of the VAT currently levied on them.

Currently, state VAT and central excise take up almost half of the retail selling price of petrol and diesel. Levying GST on them means charging a peak rate of 28% plus a fixed surcharge, with the new levy’s principal being equal to the old taxes.

GST is a consumption-based tax, and bringing petrol, diesel, and petroleum products under the regime means that states where these are sold also get the revenue. Currently, revenue is limited only to states that are production centres.

For example, populous states like Uttar Pradesh and Bihar that heavily consume these products will get more revenue at the cost of states like Gujarat.

Tax experts and financial analysts are of the opinion that this move will be a tough call for both the central and state governments. Some states will stand to lose even if products like natural gas are brought under GST as they get revenue from taxing local production and import.

The Centre government will also have to give up a majority of the ₹ 32.80 per liter excise duty on petrol and ₹ 31.80 on diesel which is not shared with state governments. Post-implementation, all revenue from these products will be equally split between the central and state governments.

The Council is also considering extending the time for duty relief on COVID-19 essentials. GST has also been reduced for COVID-19 drugs such as Remdesivir and Tocilizumab and also on items like medical oxygen and oxygen concentrators.

August

- The time limit to avail GST Amnesty Scheme has been extended till 30 November 2021. It continues to apply for GSTR-3B from July 2017 to April 2021.

- Taxpayers can get extended time up to 30 November 2021 to revoke canceled GST registration if the last date is between 1 March 2020 and 31 August 2021. This applies if the GST registration is canceled under Section 29(2) clause (b) or (c) of the CGST Act via CGST notification number 34/2021 dated August 29, 2021.

- Companies can continue to file GSTR-1 and GSTR-3B using EVC or DSC till 31 October 2021 via GST notification number 32/2021 dated August 29 2021.

- From September 1 2021, taxpayers will be unable to file GSTR-1 or use IFF for August 2021 on the GST portal if they have pending GSTR-3B filings. It applies if the filing is pending for the past two months till July 2021 (monthly filer) or for the last quarter ending June 20 2021 (quarterly filer), as per CGST Rule 59 (6).

July

- A registered person whose aggregate turnover in 2020-2021 is up to ₹ 2 Crore is exempted from filing Form GSTR-9 (annual return) for 2022-2021.

- Section 35(5) is omitted, and Section 44 is amended. This allows taxpayers to submit the reconciliation statement on a self-certification basis instead of getting it done after audit and certification by a Chartered Accountant or a Certified Management Accountant.

- Taxpayers having aggregate turnover of up to ₹ 5 Crore are not required to file self-certified GSTR-9C. Changes are notified to Form GSTR-9C from 2020-21 onwards.

June

Any late fee chargeable for non-compliance dynamic QR code requirement from 1 December 2020 to 30 September 2021 is waived off.

The following is a summary of the CBIC notification:

- The amendment of Section 50 through the 2021 Finance Act has been retrospectively notified come into effect from 1 July 2017. Interest shall now be calculated on the net tax liability after reducing eligible ITC from total liability.

- Interest and late fee relief have been extended to those who could not file GST returns by the due dates for March, April, and May 2021.

- The due date to file GSTR-1 for May 2021 has been extended from 11 June 2021 to 26 June 2021.

- The due date to file an Annual return by composition taxpayers in GSTR-4 for 2020-21 has been extended up to 31 July 2021.

- The due date to file Annual Return ITC-04 for Jan to March 2021 has been extended up to 30 June 2021.

- CGST Rule 36(4) will cumulatively apply for April, May, and June 2021 while filing GSTR-3B of June 2021.

- The time limit for completing any GST compliance (except for a few notified) falls between 15 April 2021 and 29 June 2021. This was extended to 30 June 2021.

- A new GST Amnesty Scheme has been introduced to rationalize late fees for delays in filing GSTR-3B returns from June 2021.

- The maximum late fee for GSTR-4 that can be charged will be limited to ₹ 500 per return for NIL filing and ₹ 2000 for everything other than NIL filing.

- The late fee chargeable for TDS filing under GST shall be limited to ₹ 2000, while the late fee charged per day is now ₹ 50 (down from ₹ 200)

May

The 43rd GST Council Meeting was held on 28 May 2021, and the Council approved the GST amnesty scheme to be re-introduced.

The late fee was rationalized for all taxpayers, especially for small businesses. IGST is exempted from the import of COVID treating equipment and related materials up to 31 August 2021.

Also Read: Credit Management Guide for SMBs – Things You Must Know

Conclusion

The Goods and Services Tax was introduced with the long-term vision of the country in mind. Like any other aspect of our lives, there are advantages and disadvantages of GST in India.

But, in the long term, it will lead to better prices for goods and services from a customer perspective and will also provide better income for the government, which will be used to improve the lives of the common people.

Frequently Asked Questions(FAQs)

What is the exemption limit of GST?

₹ 40 Lakhs for MSME’s and ₹ 20 Lakhs for north-eastern and hill states

What is GSTR-1?

This is a monthly or quarterly return to be filed by regular dealers. Its return is divided into 13 sections. It is the base document on top of which the compliance structure of GST is based.

If a person deals only in exempted products under their own brand, does it require registration?

No registration is required since the person only deals in exempted supplies.

What is GSTIN?

A unique identification number is assigned to a supplier or dealer. Obtaining this is absolutely free.

Is a composition dealer liable to pay a reverse charge in addition to a fixed percentage of normal GST?

If a reverse charge is applicable on a specific supply, then the composition dealer should pay GST under reverse charge as a recipient at normal GST rates.

Do businesses that provide export services need to issue a Tax invoice to customers or a bill of supply?

Exports are classified as zero-rated supplies. They have not exempted services and therefore tax invoice has to be issued.

Is GST applicable for a vegetable commission agent?

Services provided by a commission agent for the sale and purchase of agricultural produce are exempted under GST and therefore registration is not needed.

What is the current rate structure under GST?

There are four slabs in the current rate structure – 5%, 12%, 18%, and 28%.

How are imports taxed under GST?

Under the current GST regime, the Basic Customs Duty (BCD) is continued. The additional customs duty and Special Additional Duty (SAD) is replaced by IGST.

BCD paid on import is not eligible for set-off. In the case of import of services, an IGST (on a reverse charge basis) is levied, and its credit is available to the importer-recipient in accordance with the law.

10 Comments

Wow! What an amazing article! I’ve never read an article with such in-depth information on the benefits and drawbacks of GST. Please keep writing on relevant subjects.

Hello Mariam,

Thank you for your warm words.

I’m glad this article was informative to you.

Yes, I will definitely write more on pertinent themes.

Hello, can you please tell me how many different types of penalties there are for non-compliance?

Hello Cynthia,

Administrative non-compliance fines come in two varieties: fixed amount penalties and percentage-based penalties. Both of these pertain to disregarding a tax act’s administrative obligations.

Please let me know how many GST returns must be filed each month. Thanks..

Hello Vijith,

In each state where they conduct business, GST-registered companies are required to file three returns each month (GSTR-1, GSTR-2, and GSTR-3). Additionally necessary is an annual GST return.

Could you please provide me with a short overview of the GST composition scheme? Many thanks..

Hello Shweta,

For taxpayers, the GST composition Scheme is a straightforward and uncomplicated option. Small taxpayers can avoid time-consuming GST formalities by paying GST at a certain percentage of turnover instead. Any taxpayer with a turnover of less than Rs. 1.5 crore may choose this program.

Always been confused about who should be registered under GST. Your articles are greatly appreciated, absolutely love your works. Keep writing more!

Hello Nima,

Thank you very much for your kind words.

I’m happy to hear that you gained something from this article.

Keep on reading!